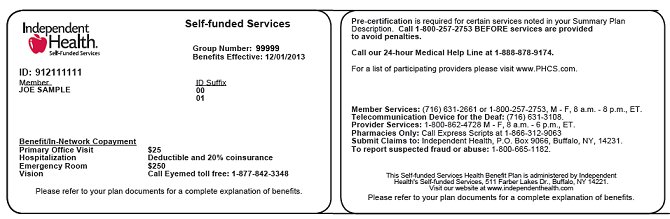

Each person covered by a health insurance plan has a unique ID number that allows healthcare providers and their staff to verify coverage and arrange payment for services. It's also the number health insurers use to look up specific members and answer questions about claims and benefits. If you're the policyholder, the last two digits in your number might be 00, while others on the policy might have numbers ending in 01, 02, etc. Many health insurance cards show the amount you will pay (your out-of-pocket costs) for common visits to your primary care physician , specialists, urgent care, and the emergency department. If you see two numbers, the first is your cost when you see an in-network provider, and the second—usually higher—is your cost when you see an out-of-network provider.

For example, when you're referred to a specific specialist or sent to a specific hospital, they may not be in your insurer's network. Coverage determinations are made on a case-by-case basis and are subject to all of the terms, conditions, limitations, and exclusions of the Member's contract, including medical necessity requirements. Health Net may use the Policies to determine whether, under the facts and circumstances of a particular case, the proposed procedure, drug, service, or supply is medically necessary. The conclusion that a procedure, drug, service, or supply is medically necessary does not constitute coverage. The Member's contract defines which procedure, drug, service, or supply is covered, excluded, limited, or subject to dollar caps.

The policy provides for clearly written, reasonable and current criteria that have been approved by Health Net's National Medical Advisory Council . The clinical criteria and medical policies provide guidelines for determining the medical necessity criteria for specific procedures, equipment and services. In order to be eligible, all services must be medically necessary and otherwise defined in the Member's benefits contract as described in this "Important Notice" disclaimer. In all cases, final benefit determinations are based on the applicable contract language.

![]()

To the extent there are any conflicts between medical policy guidelines and applicable contract language, the contract language prevails. Medical policy is not intended to override the policy that defines the Member's benefits, nor is it intended to dictate to providers how to practice medicine. If you do not see your coverage amounts and co-pays on your health insurance card, call your insurance company . Ask what your coverage amounts and co-pays are, and find out if you have different amounts and co-pays for different doctors and other health care providers.

Where Is Policy Number On Insurance Card Anthem Under the last-month rule, if you are an eligible individual on the first day of the last month of your tax year , you are considered an eligible individual for the entire year. You are treated as having the same high-deductible health plan coverage for the entire year as you had on the first day of that last month. The total contribution for the year can be made in one or more payments at any time up to your tax-filing deadline . However, if you wish to have a contribution made between January 1 and April 15 treated as a contribution for the preceding tax year, please contact the HSA bank.

If you're an HMO member, you will need to receive services from an in-network HMO provider. However, you will be able to receive emergency or urgent care services no matter where you are. For details about your coverage, please review your Blue KC certificate, which outlines the benefits and exclusions related to your health insurance plan. You can view your certificate by logging in and accessing the Plan Benefit section.

Allowable charges are the maximum amount payable to you under your health insurance plan for a particular service. Contracted providers have agreed to accept this amount as payment in full. For example, if the provider charges $100 for a service and Blue KC pays $80 as the allowable charge, the provider cannot ask the member to pay the remaining $20. Keep in mind, however, that some health insurance plans have coinsurance. In those cases, members are required to pay a percentage of the allowable charge. For specific details about your plan, review your Blue KC certificate, which outlines your payment responsibility.

There are two times you can make a change to your enrollment options. Your employer schedules an open enrollment period once a calendar year when all employees may make changes to their health insurance plan. You may also make a change during a special enrollment period if you acquire a new dependent or if your coverage is terminated under another health insurance plan. If you have health insurance through an employer, your group benefits administrator, typically someone in your Human Resources department, can help you make changes to your health insurance plan. If you do not have health insurance through an employer and instead pay your monthly premiums directly to Blue KC, call the Customer Service number listed on your member ID card. Finally, you might see a dollar amount, such as $10 or $25.

This is usually the amount of your co-payment, or "co-pay." A co-pay is a set amount you pay for a certain type of care or medicine. Some health insurance plans do not have co-pays, but many do. If you see several dollar amounts, they might be for different types of care, such as office visits, specialty care, urgent care, and emergency room care. If you see 2 different amounts, you might have different co-pays for doctors in your insurance company's network and outside the network. Once funds are deposited into your HSA, those funds can be used to pay for qualified medical expenses tax-free, even if you no longer have high-deductible health plan coverage.

The funds in your account automatically roll over each year and remain in the account indefinitely until used. Once you discontinue coverage under a high-deductible health plan and/or get coverage under another health plan that disqualifies you from an HSA, you can no longer make contributions to your HSA. However, since you own the HSA, you can continue to use it for future qualified medical expenses.

To enroll in a high-deductible health plan, complete the Blue KC application process. The Blue-Saver® PPO health insurance plan is a high-deductible health plan that allows you to establish an HSA as part of your health benefits. When you enroll in the Blue Saver plan, you may be offered the opportunity to establish a HSA with one of our preferred banks. You will be presented with appropriate banking authorizations and disclosures necessary for Blue KC to work with the bank that will establish your HSA. Once your HSA has been established, you will be mailed a welcome kit and HSA debit card from the bank. For non-emergencies, some HMO plans allow you to get health care services from a Blue Cross and Blue Shield-affiliated doctor or hospital when you are traveling outside of Illinois.

If you aren't sure, contact customer service at the number listed on your member ID card before you go. And always remember to carry your current BCBSIL member ID card. It contains helpful information for accessing health care at home or away. You cannot use HSA funds to pay for qualified medical expenses incurred before you enrolled in a high-deductible health plan. In order to establish an HSA, you must enroll in a high-deductible health plan. Your eligibility to contribute to an HSA is determined by the effective date of your high-deductible health plan coverage.

A Health Savings Account allows members enrolled in a qualified high-deductible health plan to contribute funds on a tax-free basis into the member's account. A member's employer may also contribute funds to the account. These funds are used for payment of qualified medical expenses as defined by the IRS. Unused funds in an HSA roll over in the member's account at the end of each calendar year.

To change a PCP, log in and visit you Profile by clicking on the icon by your name in the top right corner of your homepage. In the Coverage Information section you'll see a list of covered members for your Blue KC policy. From here select "Change PCP" for the appropriate member and you can search for and designate a new PCP. Once we have processed your PCP change request, we will send you a new member ID card that contains the information of your newly selected PCP.

You may also call the Customer Service number listed on your member ID card to change your PCP. Please note that if you have health insurance through your employer, you may be required to contact your group benefits administrator to change your PCP. This plan combines traditional medical coverage with a Health Savings Account .

Under this plan, all covered services (except preventive services/prescriptions) are subject to the annual deductible. The deductible is a dollar amount of out-of-pocket costs you must pay each year before the plan will begin paying its share of your healthcare expenses. The nice thing about this plan is that you can pay for that deductible using the tax-free funds in your HSA.

Once the deductible has been met, most in-network services are covered with a 20% coinsurance. If you are already seeing a specialist for your condition, make sure your doctor is in your plan's network. If the doctor is not in your plan's network, you will pay more in most cases. Also make sure your specialist uses providers and facilities in your plan's network when sending you for other services or hospitalization.

If you have any questions, call us at the customer service number listed on your member ID card. If you are looking for a doctor for your chronic condition, you can use theProvider Finder tool. Click on "Network Type" at the top and select the name of your HMO plan to see a list of doctors and hospitals in your plan's network. You can continue to use the funds in your account tax-free for out-of-pocket health expenses. If you enroll in Medicare, you can use your account to pay Medicare premiums, deductibles, copayments and coinsurance under any part of Medicare.

If you have retiree health benefits through your former employer, you can also use your account to pay for your share of retiree medical insurance premiums. The one expense you cannot use your account for is to purchase a Medicare supplement insurance or "Medigap" policy. A qualified health-deductible health plan is a health plan with an annual deductible for an individual or a family that meet the minimum deductible amount published annually by the U.S. The annual out-of-pocket expenses required by the high-deductible health plan also does not exceed the out-of-pocket maximums published by the U.S. Out-of-pocket expenses include deductibles, copayments and other amounts the member must pay for, but do not include premiums or amounts incurred for non-covered benefits.

Each payment you make for covered healthcare services you've received from your providers such as a physical exam counts toward your deductible. Once Blue KC processes the claims we receive from your providers showing the payments that you have made for covered healthcare services, we apply those payments toward your deductible. A deductible is the amount that you are responsible for paying annually for healthcare services. Exceptions are outlined in your Blue KC certificate, which lists the exclusions related to your health insurance plan. Your children's coverage while they are away from home depends on the type of health insurance plan you have. If you have health insurance through your employer, check with your group benefits administrator for more information.

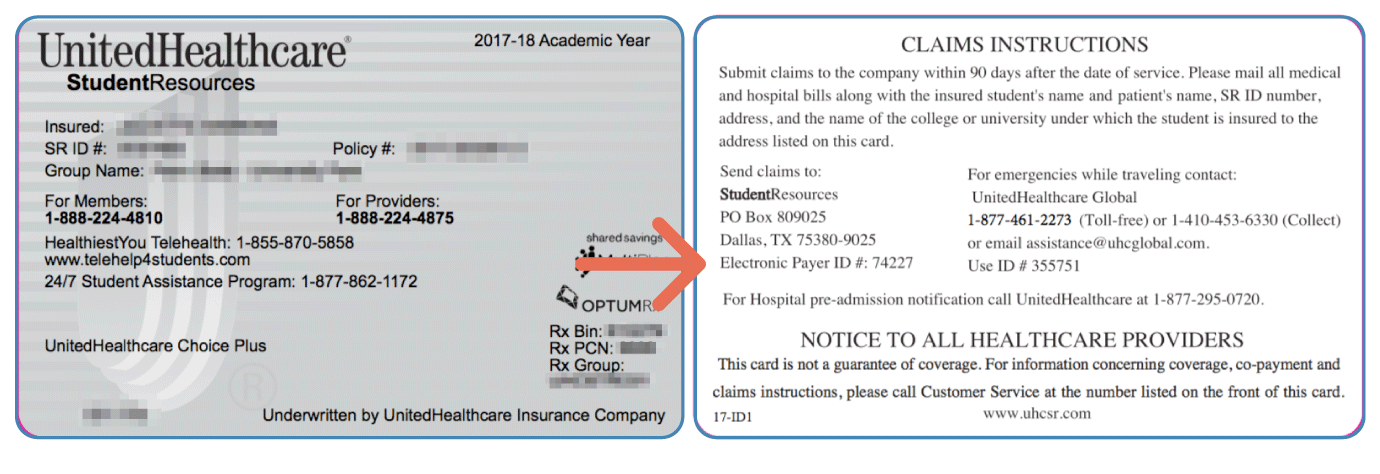

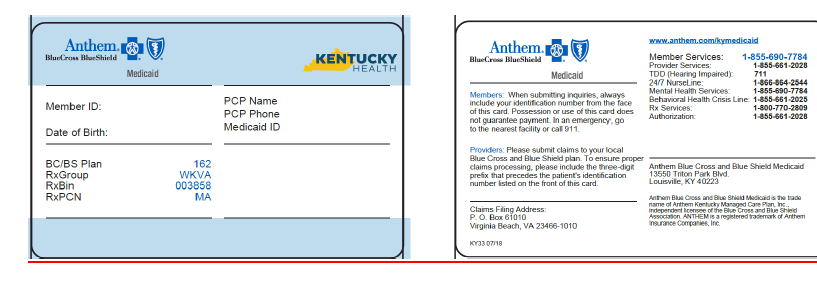

Your insurance company may provide out-of-area coverage through a different health care provider network. If so, the name of that network will likely be on your insurance card. This is the network you'll want to seek out if you need access to healthcare while you're away on vacation, or out of town on a business trip. If you lose your health insurance card with your policy and group number on it, it is important to contact your health insurance company right away and let them know. Call your insurance provider's customer service number and a representative should be able to help you.

Your health insurance policy number is typically your member ID number. This number is usually located on your health insurance card so it is easily accessible and your health care provider can use it to verify your coverage and eligibility. Beginning in 2013, Anthem Blue Cross became the behavioral health provider for Anthem HMO and PPO plans. If you are enrolled in one of these Anthem plans, you do not need a referral from your primary care physician in order to receive mental health services. Visit Anthem's website at /ca for a list of behavioral health providers.

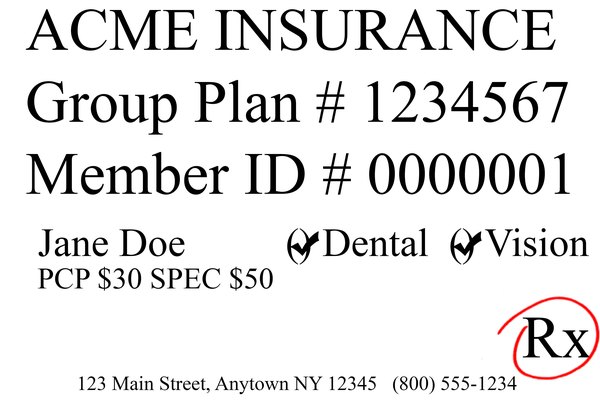

Your health insurance company might pay for some or all the cost of prescription medicines. If so, you might see an Rx symbol on your health insurance card. But not all cards have this symbol, even if your health insurance pays for prescriptions. Sometimes, the Rx symbol has dollar or percent amounts next to it, showing what you or your insurance company will pay for prescriptions.

If you have health insurance through your employer, check with your group benefits administrator to have a dependent added to your plan. He or she has the information and/or forms you need to add your dependent to your health insurance plan. Show your ID card every time you visit the doctor, pharmacy, hospital, or any other healthcare provider.

Healthcare providers can use your member ID number to review your benefits, and can let you know if you owe any copayments at the time of your visit. You might see another list with 2 different percent amounts. The back or bottom of your health insurance card usually has contact information for the insurance company, such as a phone number, address, and website.

This information is important when you need to check your benefits or get other information. For example, you might need to call to check your benefits for a certain treatment, send a letter to your insurance company, or find information on the website. If you have health insurance through work, your insurance card probably has a group plan number.

The insurance company uses this number to identify your employer's health insurance policy. If you forget or aren't sure what type of health insurance plan you have , you can find out on your BCBS ID card. If you have an HMO, your card may also list the physician or group you've selected for primary care. Determining whether a provider is in-network is an important part of choosing a primary care physician. Centura Health accepts and bills most major insurance companies as a source of payment.

However, some of their benefit plans do not cover treatment at some Centura Health locations. It is recommended that you contact your insurance company directly if you have any questions about coverage at a Centura Health location. Routine Preventive care is a care benefit that is not subject to a deductible. A copayment, or copay, is the dollar amount that you pay to a provider at the time you receive a service. For example, you might pay a $30 copay each time you visit your allergy doctor. The copay amount is defined in your Blue KC certificate, which outlines your responsibilities for health insurance plan payments.

When you elect the Anthem PPO HDHP, you are also eligible to elect a Health Savings Account , a special tax-advantaged bank account to help cover your out-of-pocket healthcare costs. The descriptions below apply to most private health insurance ID cards in the United States. If you live outside the U.S. or have government-provided insurance, you may see some different fields on your card. If you have family members listed as dependents on your health insurance plan, they may each have their own unique policy number as it is used for identification purposes and billing procedures. Your health insurance policy number is what identifies you as a covered individual under your current or previous plans. It's important because if you change jobs or get married, divorced, etc., then your HIPN will need to match the new situation.

If you move out of state, your HIPN needs to reflect where you live now. Your first premium payment activates your coverage, so you can start using your health plan within 1–2 days of making your payment, depending on how you pay. After you've made your first payment and your coverage is activated, you can have health care expenses during that coverage gap applied to your deductible, or even get paid back for some services. In this case, the coverage gap would be the time between your requested effective date and the date you make your first payment. The "coverage amount" tells you how much of your treatment costs the insurance company will pay. This information might be on the front of your insurance card.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.